Fintech Solutions

Back Testing System

Our Back Testing System enables traders, brokers, and institutions to validate trading strategies against historical market data before deploying them in live environments. This helps eliminate guesswork and ensures data-driven decision-making.

The system supports multi-year historical datasets, multiple timeframes, and asset classes including Equity, Futures, and Options. Users can analyze key performance metrics such as profitability, drawdowns, win ratios, and risk exposure.

Advanced analytics and visualization tools allow users to fine-tune strategies by adjusting parameters and instantly viewing results. This significantly reduces strategy failure rates in live markets.

Built with scalability and accuracy in mind, our back-testing engines are designed to handle large datasets with high precision, ensuring reliable and actionable insights.

Custom Strategies

We specialize in designing and developing custom trading strategies tailored to specific business goals, trading styles, and risk profiles. Each strategy is aligned with client-defined rules, indicators, and execution logic.

Our team works closely with clients to translate trading ideas into structured, automated strategies across Equity, F&O, and options-based models. Strategies can be discretionary, rule-based, or fully algorithmic.

Risk management, capital allocation, and position sizing are embedded into every strategy to ensure controlled exposure and regulatory alignment.

All strategies are delivered with thorough testing, documentation, and optimization support to ensure a smooth transition from concept to live trading.

Algo Trading Platforms

Our Algo Trading Platforms are built for speed, stability, and scalability, enabling fully automated trade execution with minimal latency. These platforms eliminate manual intervention and ensure precise order placement.

The platform includes strategy management, real-time monitoring, order routing, and fail-safe mechanisms. It supports high-frequency, intraday, and positional trading models.

Designed with modular architecture, our systems easily integrate with broker APIs, OMS, RMS, and exchange feeds. This ensures seamless data flow and operational efficiency.

Security, reliability, and performance are core priorities, making our algo platforms suitable for retail brokers, prop desks, and institutional traders.

Equity & F&O Price Alerts

Our real-time price alert system ensures traders and investors never miss critical market movements. Alerts are generated instantly based on predefined price levels, conditions, or technical triggers.

The system supports Equity, Futures, and Options instruments with configurable thresholds and smart conditions. Alerts can be delivered via web, mobile, email, or messaging platforms.

This helps users react quickly to market opportunities without continuously monitoring screens. Alerts improve execution timing and overall trading efficiency.

The solution is highly scalable and can be customized for individual traders, broker clients, or enterprise-wide deployments.

IV Alerts (Implied Volatility)

IV Alerts are designed to help options traders identify volatility opportunities in real time. The system continuously monitors implied volatility across contracts and strikes.

Alerts are triggered when volatility deviates from historical norms or crosses defined thresholds, enabling traders to act proactively on market sentiment changes.

This solution is ideal for options writers, spread traders, and volatility-based strategies. It enhances timing accuracy and risk awareness.

The IV engine integrates seamlessly with options analytics platforms and trading systems for a unified trading experience.

Post Trade Risk Management System (RMS)

Our Risk Management System provides real-time control over trading exposure, margins, and limits to safeguard capital and ensure compliance.

The RMS continuously monitors positions, orders, and margins across segments, enforcing predefined rules before and after trade execution.

It helps brokers and trading firms prevent excessive risk, unauthorized trades, and regulatory breaches through automated checks and alerts.

Designed to meet exchange and regulatory standards, the system is scalable, configurable, and suitable for high-volume trading environments.

NSE / BSE Integrations

We offer robust and secure integrations with NSE and BSE for market data feeds, order management, and drop copy services.

Our integration layer ensures low-latency data flow, high availability, and accurate synchronization with exchange systems.

This enables brokers and fintech platforms to build reliable trading, reporting, and surveillance solutions.

All integrations are developed following exchange protocols and compliance requirements to ensure operational continuity.

Wealth Management Platform

A Wealth Management Platform is a comprehensive digital ecosystem that empowers financial advisors, wealth managers, family offices, and investment firms to efficiently manage client portfolios, financial planning, investment advisory, and relationship management.

The platform provides real-time portfolio tracking, multi-asset investment management, risk assessment, compliance monitoring, and advanced analytics, enabling organizations to deliver personalized wealth-building strategies while enhancing operational efficiency and client satisfaction.

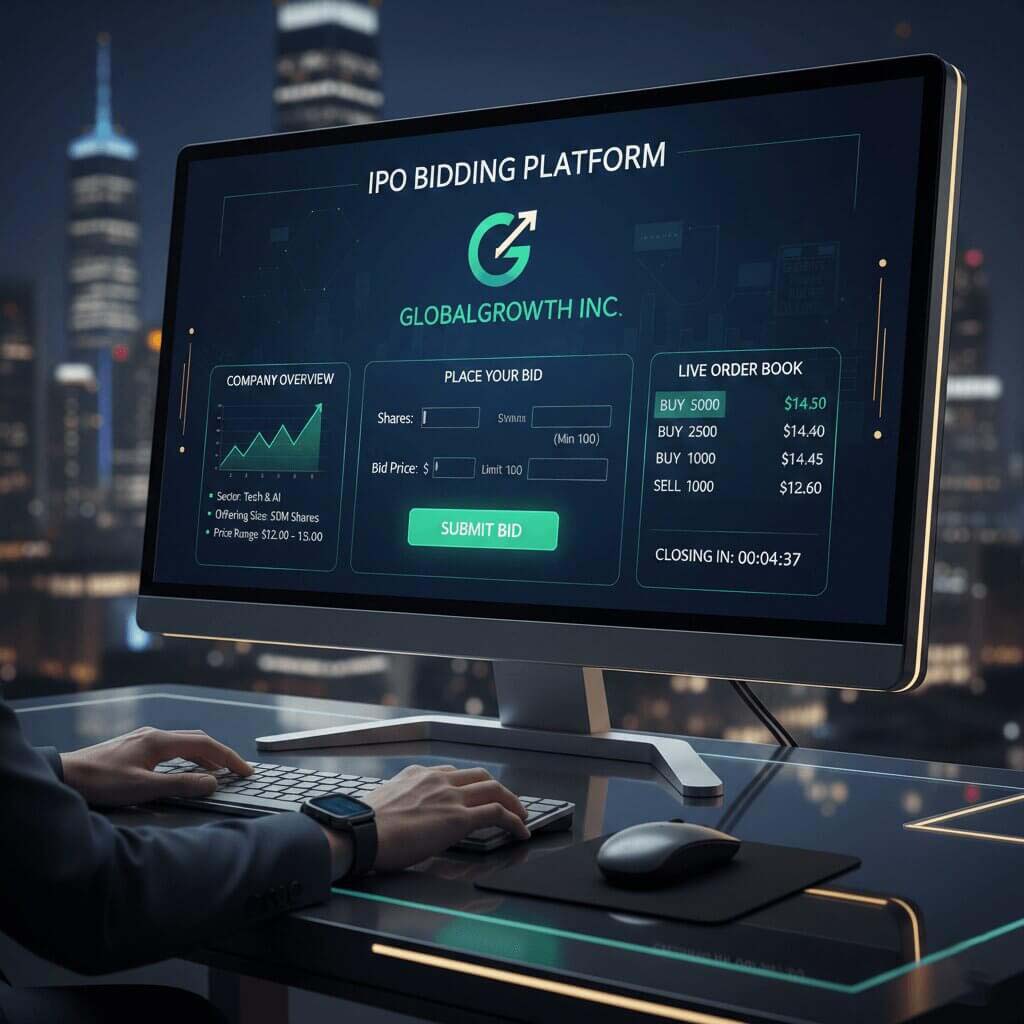

IPO Bidding Platform

Our IPO Bidding Platform provides a seamless and secure experience for investors to participate in public offerings digitally.

The platform supports bid placement, modification, cancellation, and real-time status tracking with exchange connectivity.

It integrates with banking, depository, and broker systems to ensure smooth mandate handling and allotment workflows.

This solution helps brokers increase IPO participation while ensuring regulatory compliance and operational efficiency.

Mutual Fund Platform

Our Mutual Fund Platform enables end-to-end digital investment management for distributors, brokers, and investors.

The system supports SIPs, lump-sum investments, redemptions, switches, and portfolio tracking across AMCs.

Integrated reporting, compliance, and transaction tracking ensure transparency and ease of use.

The platform is scalable, secure, and designed to enhance investor experience while simplifying backend operations.

PMS Platform

Our PMS Platform empowers portfolio managers with advanced tools for managing client investments efficiently.

It offers real-time portfolio valuation, performance analytics, and detailed reporting for investors.

Compliance, audit trails, and regulatory reporting are built into the platform to meet SEBI requirements.

The solution enhances transparency, improves client trust, and streamlines portfolio operations.

Stock Market Hints

Our Stock Market Hints solution delivers intelligent, data-driven trade insights to support informed decision-making.

Hints are generated using technical indicators, historical analysis, and real-time market data.

This service helps traders identify potential opportunities while maintaining disciplined risk management.

It can be integrated into client portals, mobile apps, or advisory platforms.

Client Portal

Our Client Portal provides a secure, user-friendly interface for investors to access their trading and investment data.

Clients can view portfolios, transaction history, reports, alerts, and performance metrics in real time.

Role-based access ensures data security and personalized user experiences.

The portal strengthens client engagement and improves transparency between brokers and investors.

Customized Development

We offer fully customized fintech and trading solution development tailored to unique business requirements.

From concept and architecture to development and deployment, we handle the complete lifecycle.

Our solutions are built using modern technologies, scalable architectures, and secure APIs.

This ensures future-ready platforms that grow with your business and evolving market needs.